When it comes to running a business, you may find yourself completing tasks that you’re just not used to. Whether it’s organising your finances, hiring new employees or dealing with taxes, being self-employed carries a number of big responsibilities.

With the April 2020 deadline looming for Making Tax Digital, one of the biggest challenges for businesses can be keeping track of their records. How can you store them safely? Where is the best place to store them? And how long should you keep business records? Read on to find out…

According to Gov.uk, all limited companies must keep their records for at least six years from the end of the last company financial year that they relate to. You must keep records that include:

If you fail to keep all relevant financial records, you can be fined £3,000 by HMRC and can be disqualified from being a company director.

If you’re self-employed, rather than the owner of a limited company, the rules are a little different. You must keep records for at least 5 years after the last submission deadline of the relevant tax year. These records may be checked to ensure you are paying the right amount of tax.

For both self-employed and limited company records, you must recreate any documents you can if they are lost, stolen or destroyed. You must also alert HMRC straight away so they can make a note on your record.

With the new GDPR legislation in place, it’s more important than ever to make sure all employee records are secured safely and protected. Accident records, income tax, national insurance documents, salary and pay and recruitment records all typically need to be stored for anywhere between 6 months to 3 years. Wherever possible, it’s best to store them for longer.

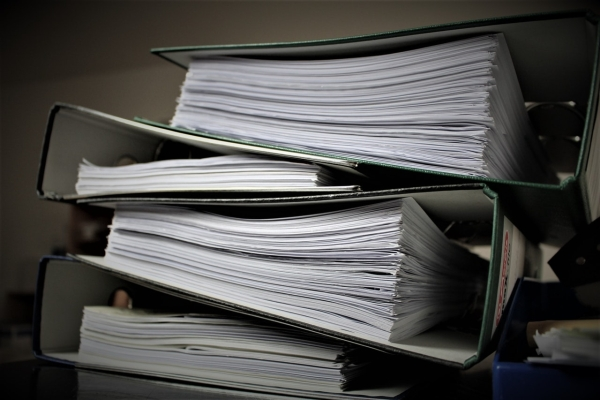

Physical financial statements and employee records will soon stack up when you need to keep them for several years. On top of that, paper records pose significant issues when it comes to security and GDPR.

That’s why it’s important to have a secure digital system to keep them safe and easy to access without cluttering your office space. Digital asset management allows you to store all your business records in one central spot and can restrict access to any employees that do not have authority to view the files.

With iBase’s metadata system, you can make sure all tax records, for instance, are easily retrievable, saving you a great deal of time at the end of each financial year. Even better, with advanced security systems, you will be fully compliant with GDPR.

To find out more about how iBase’s DAM system can help you, get in touch with us today.